Second Home Loans In The Outer Banks Real Estate Market

I saw an article recently that caught my eye, actually the headline did.

"Demand For Vacation Homes Is Down More Than 50% From Pre-Pandemic Levels"

https://www.redfin.com/news/demand-down-second-homes-march-2023/

It made me wonder if people are avoiding short term rentals due to the wording, but that's not what the article is about. Mortgage rate locks for second homes are down 52% and this doesn't surprise me at all. As a real estate agent in a vacation area, I can see a real slowdown in activity. Some of that is due to a lack of inventory but the majority of it in my opinion is due to two factors that are symbiotic in nature.

1) When FHFA adjusted fees higher for second home loans in the spring of 2022, that alone put an obvious damper on borrowing activity. In my area this equates to a "hidden" 0.5%-1% difference in the rate offered on 2nd home vs primary home loans (assuming both homes are conforming/conventional loans that can be resold). CoreLogic did an article on this in September last year and you can clearly see the drop in demand.

2) Couple that with the fastest Fed rate hikes measured in the last 35 years, starting in March of 2022. This caused mortgage rates to quickly rise, and buyers looking at a conforming loan were facing the double edged sword of the "hidden" rate hike plus higher rates than at any point since March of 2020. The average 30 year mortgage then quickly spiked from 3.22% in January 2022 all the way up to 6.95% in November of 2022. And this is the average 30-year mortgage tracked by the Fed-

https://fred.stlouisfed.org/series/MORTGAGE30US

This is not the average 2nd home mortgage, that would have shown an even BIGGER spike from January to November of last year.

There was a small window of time when jumbo and portfolio loans were much lower rates, since they wouldn't be resold to Fannie or Freddie. But with the Fed continuing to hike rates, even those went up. Further damaging the carrying costs of a mortgage on a second home was the continued rise in home prices. In areas with limited supply (like a barrier island) and high demand, it has resulted in a higher $ per sq ft being paid in 2023 vs 2022 on the Outer Banks among completed sales. But buyers are opting for homes in the $300-500k range and aren't as interested in homes in the $800k range thanks to another change from federal housing authorities.

When the conforming loan limit was raised to $726,200 for 2023, anyone buying an $800k house with 20% down would end up below the conforming loan limit.

https://themortgagereports.com/27773/2017-conforming-mortgage-loan-limits-fannie-mae-freddie-mac

So if homes cost more, and carrying costs for mortgages cost more, and buying a second home is penalized due to FHFA regulations, why wouldn't mortgage demand for vacation rentals drop significantly vs a time period when there was no "hidden" surcharge and the average 30-year fixed rate conforming 2nd home loan was around 4.25%?

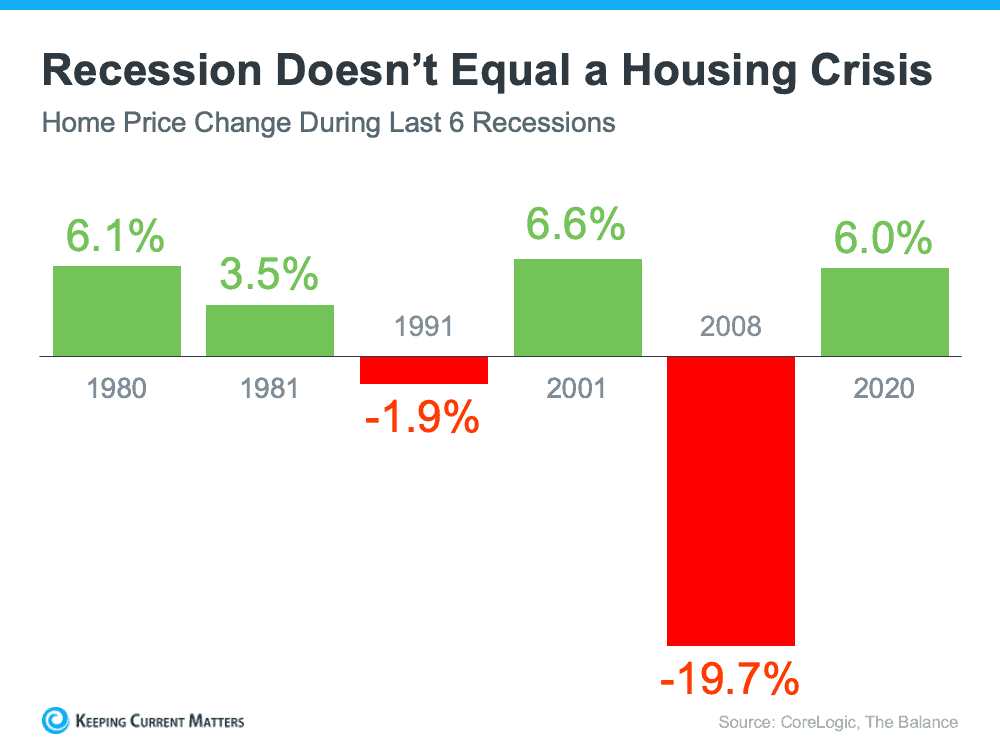

We haven't seen foreclosures like we did in 2007-2008 because homeowners today have plenty of equity after price gains of the last 2 years. Owners can do a cash-out refinance, list the house, rent the house out, they have tons of options compared to 2007-08. If a homeowner needs to sell, he can price the home to sell and there's no shortage of buyers. But there IS a shortage of buyers willing to pay current mortgage rates. I worry that homebuyers will start resorting to ARMs rather than fixed-rate mortgages to get some relief from today's mortgage rates, and I think the standard 30-year mortgage is very important for stability in the housing market.

Further complicating matters is that the Federal Reserve has essentially put a cap on a soda and shaken it - injected energy into it that wasn't otherwise there - and when they remove the lid (and lower rates again) all of that excess energy will propel a tsunami of homebuyers back into the housing market, driving home prices up even more. I talk to plenty of people who say they are just waiting for rates to come down. And most current owners with locked-in 3% mortgages (before the "hidden" surcharge for second home ownership) have no real incentive to sell their house - so who will be listing their homes for sale? And if sellers aren't willing to give up their 3% mortgages, knowing they will never get a second home loan at 3% again, how much inventory can come back to the market?

Real estate is still about basic supply and demand. The rapid rate hikes only injected external energy into the buyer demand equation. Buyers are lined up and waiting for rates to drop. But the FHFA/Fannie/Freddie second home changes will keep many owners locked into their homes long-term. And with lots of demand and very little supply, I think we all know what will happen when mortgage rates drop again.

And I don't think it will benefit the people that the FHFA claims it has a "core mission" to serve - primary homeowners and first time buyers. They will suffer the most from rising home prices and competition from investors who suddenly see a 5% rate as a bargain. I think the FHFA and the Federal Reserve have set the stage for another "gold rush" in the housing market as soon as mortgage rates fall. Which according to the bond market, is likely to start as soon as fall of 2023.

Categories

Recent Posts

“Looking for more information? Just fill out some details and let me know how to connect with you! ”